Private Equity Market Size, Share, Trends & Outlook Report, 2034

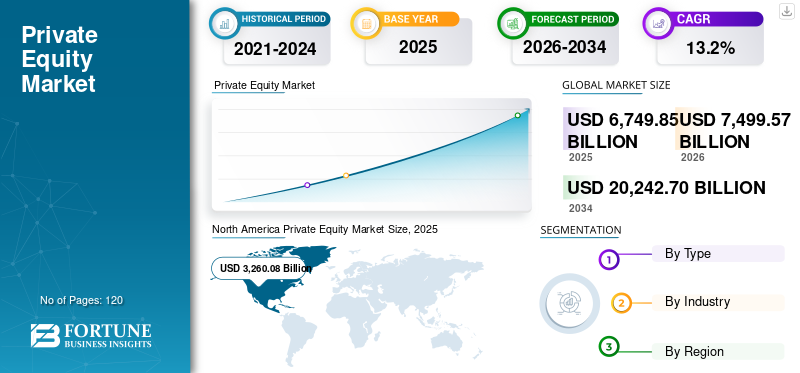

The global private equity market is poised for significant expansion, with its valuation expected to grow from $6,749.85 billion in 2025 to over $20,242.70 billion by 2034 at a compound annual growth rate of 13.2%. This growth is underpinned by sustained institutional capital inflows from pension and sovereign wealth funds, which are increasingly allocating 10% to 20% of their portfolios to the asset class. As exit environments remain complex, the industry is shifting toward operationally driven value creation and the strategic use of secondary markets to manage liquidity.

North America remains the dominant force in the sector, accounting for 48.3% of the global market share as of 2025, while total assets under management are expected to exceed $7 trillion. Major industry players including Blackstone, KKR & Co., Apollo Global Management, The Carlyle Group, and TPG are aggressively scaling diversified platforms to target high-growth sectors like technology, healthcare, and infrastructure. While fundraising has moderated from previous peaks, capital remains concentrated among established managers with proven track records, as investors prioritize operational capabilities and specialized domain expertise to navigate evolving market conditions.

A significant trend reported is the convergence of private equity and private credit, with sponsors increasingly utilizing non-bank lenders for large-cap leveraged buyouts and refinancings. To navigate a slower exit environment, firms are turning to continuation vehicles and secondary transactions, allowing limited partners to achieve liquidity while sponsors maintain exposure to high-performing assets. These custom capital stacks, including unitranche and PIK notes, are supporting longer holding periods and providing flexible financing solutions that allow companies to remain private for longer durations while maintaining influence over strategic direction.

The industry is undergoing a fundamental transition from relying on leverage and multiple expansion toward operationally driven value creation. General partners are building in-house operating teams focused on digital transformation, margin improvement, and revenue acceleration to enhance portfolio performance. Furthermore, the integration of advanced data analytics and standardized ESG frameworks into the investment lifecycle is becoming a requirement for modern deal sourcing, due diligence, and risk management, ensuring that firms can identify operational inefficiencies early in the investment cycle.

Summary generated by RabbitReport AI from public reporting. The full article and original reporting belong to Fortune Business Insights.