Remittance Market Size, Share | Industry Report [2026-2034]

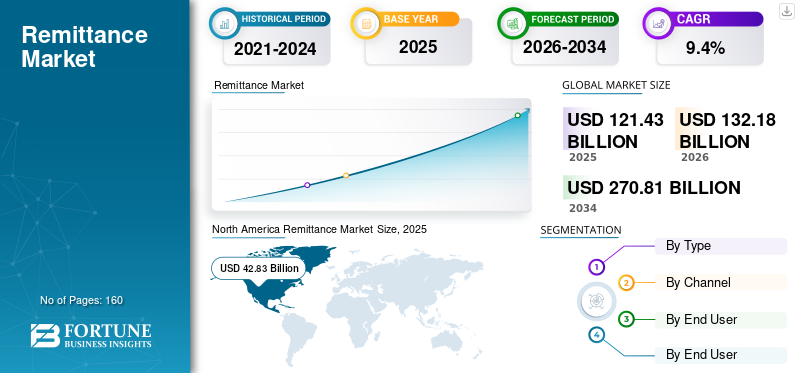

The global remittance market, valued at $121.43 billion in 2025, is expected to experience significant growth driven by a 9.4% CAGR through 2034. This expansion is fueled by increasing international migration, the widespread adoption of smartphones, and a shift from traditional cash-based transfers to low-cost digital platforms. For the payments sector, this trend underscores a critical transition toward instant payment infrastructures and fintech-led competition that is reshaping cross-border money movement.

The global remittance industry is set to grow from $132.18 billion in 2026 to $270.81 billion by 2034, exhibiting a CAGR of 9.4%. North America currently leads the market, generating $42.83 billion in revenue and holding a 32.27% share in 2025. Key industry players including Western Union, MoneyGram, PayPal, and Wise are leveraging strong physical networks and seamless digital integrations to maintain their competitive edge. While traditional bank transfers currently hold the highest market share due to established trust and regulatory compliance, online and digital platforms are expected to witness the highest growth rate as users prioritize lower fees and real-time tracking.

Growth is being propelled by strengthening remittance corridors, such as the U.S.-Mexico route, and a rising migrant workforce in regions like Asia Pacific, which reached $26.25 billion in 2025. The outward remittance segment remains dominant as expatriates send money for household expenses, education, and healthcare, while inward remittances are projected to grow at a 9.7% CAGR. This shift is supported by government initiatives to reduce cash dependency and the integration of APIs and automated settlement mechanisms that enhance transaction speeds and customer experience. Increasing smartphone penetration and improved internet access are also cited as prominent factors driving the shift toward digital wallets and mobile apps.

Despite the positive outlook, the sector faces hurdles including stringent KYC requirements, exchange rate volatility, and rising cybersecurity threats such as phishing and identity theft. These risks can undermine consumer trust and lead to direct financial losses, potentially slowing the adoption of digital platforms. To mitigate these risks and improve financial inclusion, service providers are increasingly linking instant payment infrastructures to enable seamless, low-cost cross-border transactions. As governments support interoperable payment frameworks, the industry is moving toward a more transparent model that reduces reliance on traditional intermediaries and expands access to underbanked populations.

Summary generated by RabbitReport AI from public reporting. The full article and original reporting belong to Fortune Business Insights.