Military Edge Computing Market Size, Share | Growth [2034]

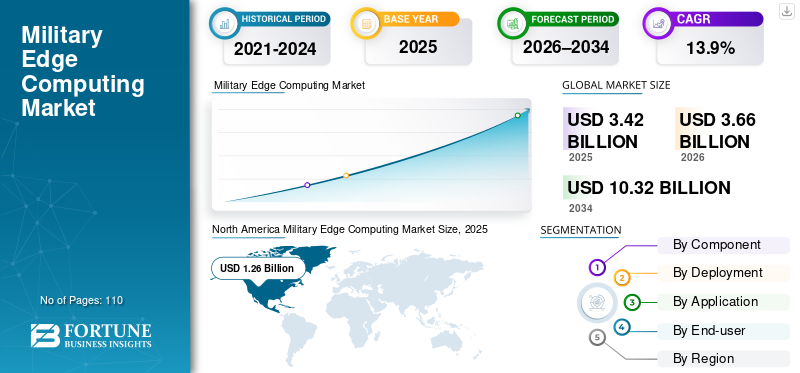

The global military edge computing market is forecast to grow from $3.42 billion in 2025 to $10.32 billion by 2034, representing a compound annual growth rate of 13.9%. This expansion is driven by the increasing need for real-time data processing and autonomous operations in contested environments where low-latency situational awareness is critical. North America currently leads the sector, accounting for a 36.84% market share as defense agencies prioritize distributed computing architectures and AI-driven analytics.

The military edge computing sector is experiencing significant growth as defense organizations transition toward multi-domain operations and AI-driven analytics. Valued at $3.42 billion in 2025, the market is expected to reach $10.32 billion by 2034, fueled by the integration of sensor data from unmanned systems, ISR assets, and electronic warfare equipment. Key industry players, including Lockheed Martin, General Dynamics, Microsoft, and Raytheon Technologies, are focusing on enhancing processing power and cyber-resilience at the tactical edge. These advancements allow for local data analysis that supports both human operators and autonomous platforms in austere environments where resilience is essential.

A major trend within the market is the integration of embedded and generative AI to facilitate real-time predictive insights without relying on centralized servers. Generative AI enables commanders to simulate scenarios and optimize mission planning locally, which is vital in communications-denied or contested environments. Furthermore, the land segment dominated the market in 2025 with a 50.6% share, driven by the deployment of mobile command units and ground robots that perform AI inference on-board. These systems analyze sensor feeds and environmental inputs to enable adaptive route planning and rapid target recognition while reducing dependence on continuous communication links or operator intervention.

Global defense modernization programs are serving as primary catalysts for edge computing adoption. In the United States, initiatives like the Joint All-Domain Command and Control (JADC2) and the Next Generation Combat Vehicle program are implementing distributed architectures to shorten sensor-to-shooter timelines. Similar efforts are underway in Europe and the Asia Pacific region to enhance multi-domain interoperability and resilient communications. However, the sector faces technical challenges related to connectivity and bandwidth limitations, as hostile conditions such as electronic jamming and limited spectrum availability can disrupt the intermittent data exchange required for distributed sensor fusion and autonomous vehicle coordination.

Summary generated by RabbitReport AI from public reporting. The full article and original reporting belong to Fortune Business Insights.