Marine Fuel Optimization Market Projected to Reach Nearly $3 Billion by 2034

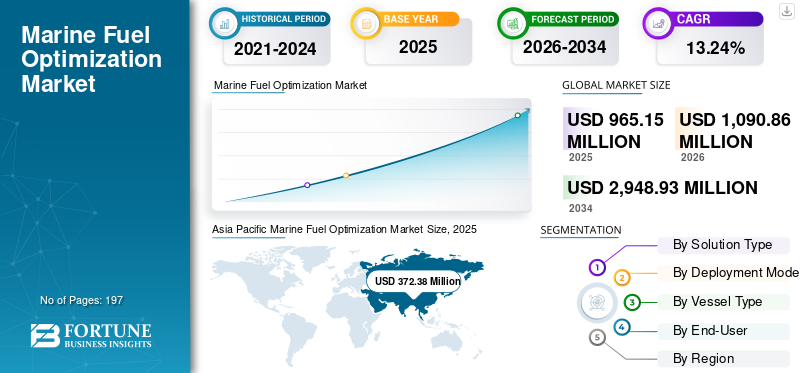

The global marine fuel optimization market is projected to grow from $965.15 million in 2025 to approximately $2.95 billion by 2034, driven by a compound annual growth rate of 13.24%. This expansion is fueled by the maritime industry's need to mitigate rising fuel costs and comply with increasingly stringent international environmental regulations aimed at reducing greenhouse gas emissions. As the sector embraces digitalization, the integration of real-time data analytics and smart shipping technologies is becoming essential for maintaining operational efficiency across global fleets.

The global marine fuel optimization (MFO) market is experiencing a significant upward trajectory, with the Asia Pacific region leading the sector with a 38.58% market share in 2025. These systems represent a critical shift in maritime operations, moving away from traditional fuel management toward advanced digital platforms that utilize real-time data analytics, engine performance monitoring, and weather routing. By leveraging onboard sensors and cloud-based analytics, MFO solutions provide ship operators with precise insights into vessel performance, which is vital for commercial shipping, offshore vessels, and naval operations. The market is expected to reach $2,948.93 million by 2034 as these technologies become standard components of modern maritime digitalization.

The primary drivers for the adoption of MFO solutions include the high cost of fuel, which constitutes a major portion of vessel operating expenses, and the necessity of meeting global sustainability standards. Advancements in artificial intelligence, the Internet of Things (IoT), and predictive analytics are enabling more accurate fuel management, allowing operators to optimize voyage planning and speed. These tools are increasingly necessary as global trade volumes grow and shipping companies manage larger, more complex fleets that require centralized monitoring and cross-fleet standardization. Regulatory pressure to improve energy efficiency is further compelling shipowners to invest in these intelligent systems to reduce operational risks and carbon footprints.

The competitive landscape is moderately fragmented, featuring major technology providers such as Wärtsilä Corporation, Kongsberg Gruppen, ABB Ltd., DNV, and Siemens Energy alongside specialized regional vendors. In 2025, industry giants Maersk and Hapag-Lloyd expanded their use of digital fleet optimization platforms, while CMA CGM integrated data-driven systems to enhance fleet efficiency. Technology providers are increasingly collaborating with shipping companies to deploy AI-enabled voyage optimization and performance analytics. These strategic initiatives, combined with a focus on integrating onboard systems with cloud platforms, are shaping the future of the market and supporting long-term growth in the maritime technology sector.

Summary generated by RabbitReport AI from public reporting. The full article and original reporting belong to Fortune Business Insights.