AI in Pharma and Biotech Market Size, Share | Growth [2034]

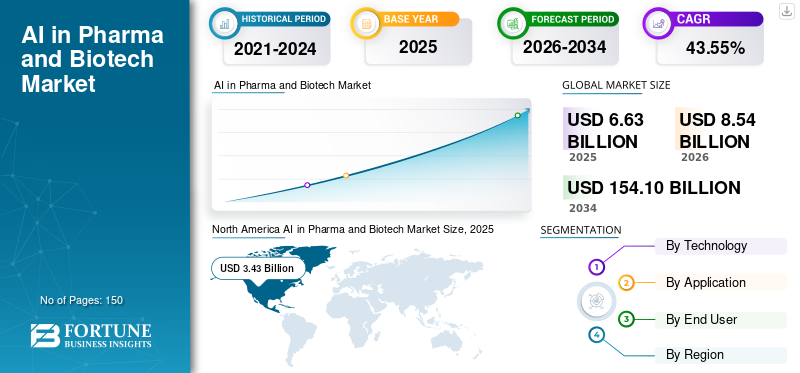

The global market for artificial intelligence in the pharmaceutical and biotechnology sectors is poised for explosive growth, expanding from an estimated $6.63 billion in 2025 to over $154 billion by 2034. This rapid expansion, characterized by a compound annual growth rate of 43.55%, is driven by the transition of AI from experimental pilots to integrated production workflows across drug discovery and clinical operations. As the industry prioritizes repeatable returns on investment, the adoption of generative AI for molecular design and de-novo chemistry is becoming a central pillar of modern research and development strategies.

The global AI in pharma and biotech market is undergoing a massive transformation, with North America leading the sector through a 51.73% market share valued at $2.43 billion in 2025. Machine learning and deep learning technologies currently dominate the landscape due to their ability to process high-dimensional data such as omics, imaging, and high-throughput screening. Key industry players, including Insilico Medicine, Recursion, and IBM, are increasingly focusing on production-grade foundations and clean data pipelines to ensure models perform reliably over time. This shift is particularly evident in the drug discovery and development segment, which is projected to hold a 29.8% market share by 2026 as firms integrate AI directly into their development pathways.

A primary driver for this growth is the wider adoption of generative AI for molecular design, which allows researchers to propose novel molecules rather than simply screening existing libraries. This technology supports multi-objective optimization, improving lead quality and reducing the time required for hit-to-lead transitions. However, the increasing complexity of these models has created a significant demand for cloud providers and high-performance computing (HPC) specialists, as many research teams cannot scale using on-premise resources alone. These partnerships are essential for reducing upfront capital expenditures and shortening procurement cycles, allowing R&D teams to utilize specialized AI accelerators for faster screening and simulation.

Despite the optimistic growth projections, the industry faces significant hurdles related to regulatory validation and technical integration. Regulators require clear evidence of data provenance, model performance, and bias controls before AI-generated outputs can influence clinical decisions, which often adds time and cost compared to traditional workflows. Furthermore, integrating AI platforms with fragmented existing systems like Electronic Lab Notebooks (ELN) and Laboratory Information Management Systems (LIMS) remains a major challenge. Nevertheless, pharmaceutical and biotechnology companies continue to lead spending, expected to hold a 54.9% share of the end-user market in 2026, while Contract Development and Manufacturing Organizations (CDMOs) and Contract Research Organizations (CROs) are also projected to see robust growth with a CAGR of 43.31%.

Summary generated by RabbitReport AI from public reporting. The full article and original reporting belong to Fortune Business Insights.