Global Fleet Management and Mobility Services Market Expected to Reach $218.96 Billion by 2034

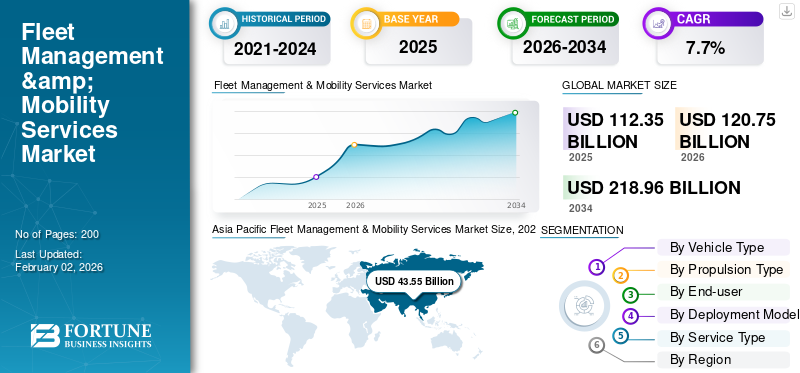

The global fleet management and mobility services market is projected to grow from $112.35 billion in 2025 to $218.96 billion by 2034, exhibiting a compound annual growth rate of 7.7%. This growth is primarily driven by the integration of digital platforms that manage vehicle fleets while providing shared, on-demand transportation solutions to improve efficiency and cost control. For the fleet management sector, this shift signifies a major move toward electrification and data-driven operations, particularly in the Asia Pacific region, which currently accounts for nearly 39% of the global market.

The market expansion is being propelled by the adoption of artificial intelligence, IoT sensors, and advanced data analytics, which allow for predictive maintenance and automated compliance reporting. Industry leaders like Verizon Connect, Geotab, Trimble, Samsara, Omnitracs, and Fleet Complete are leveraging these technologies to help operators manage rising fuel and labor costs through real-time tracking and route optimization. This focus on cost-efficiency is accelerating the adoption of fleet management solutions across logistics, public transport, and shared mobility sectors globally, as companies seek to reduce downtime and improve asset utilization.

On a segment basis, while internal combustion engine (ICE) vehicles maintain the largest market share due to their massive global installed base, electric vehicles (EVs) represent the fastest-growing propulsion type with a 17.7% CAGR. This transition requires new management capabilities for monitoring battery health, charging schedules, and energy consumption. Similarly, while passenger cars remain the dominant vehicle type due to high penetration in corporate fleets and ride-hailing, the two-wheelers and micro-mobility segment is growing at 10.0% annually, fueled by the rapid expansion of last-mile delivery and urban congestion management strategies.

Despite the strong growth outlook, the industry faces significant barriers including high upfront costs for hardware and software licenses, which can hinder adoption among small and medium-sized fleet operators. Additionally, the continuous collection of vehicle and driver data necessitates robust cybersecurity measures and strict adherence to privacy regulations to prevent cyberattacks and maintain user trust. Addressing these financial and technical challenges, alongside the integration of legacy IT systems, will be crucial for service providers as they look to scale operations across diverse and cost-sensitive global markets.

Summary generated by RabbitReport AI from public reporting. The full article and original reporting belong to Fortune Business Insights.