Insurance now eats up 8.5% of housing costs: report

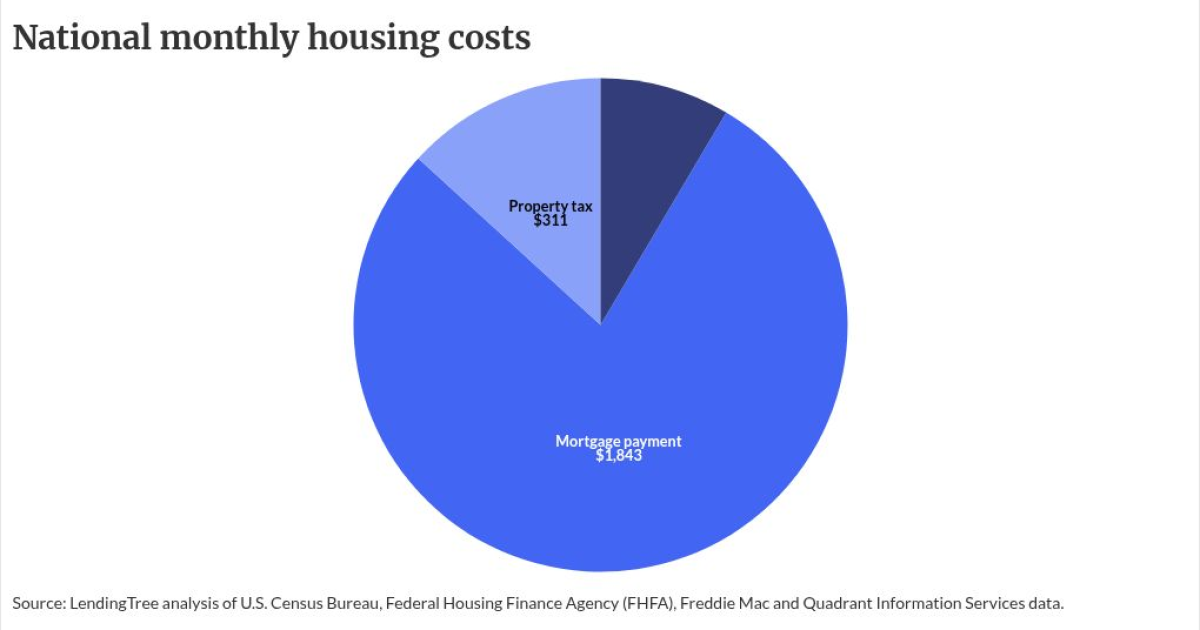

A new report from LendingTree reveals that homeowners insurance now accounts for 8.5% of typical monthly housing costs across the United States, driven by extreme weather events and persistent inflation. This financial shift means the average homeowner with a mortgage pays approximately $200 per month for coverage out of a total $2,354 housing bill. For the property insurance sector, these findings highlight how rising premiums are increasingly dictating consumer purchasing power and rivaling property taxes as a primary expense in several states.

According to data analyzed by LendingTree, home insurance costs have reached a point where they represent 10% or more of monthly housing expenses in 20 different states. Nebraska leads the nation with insurance taking up 19.4% of housing costs, followed by Oklahoma at 17.6% and Texas at 14.4%. LendingTree insurance analyst Rob Bhatt noted that while insurance was once an afterthought for homebuyers, it now exerts an outsized influence on buying power, particularly in regions prone to severe wind, hail, and tornadoes where carriers have priced potential disaster costs into their rates.

The report highlights significant regional disparities in premium totals, with Colorado homeowners paying the highest average premium at $463 per month, or $5,553 annually, due to frequent wildfires and hailstorms. In 15 states, including Tennessee, Nebraska, and Oklahoma, the cost of insurance has actually surpassed property tax bills. In Tennessee specifically, homeowners spend an estimated $284 monthly on insurance, which is nearly double the state’s average property tax of $143. This trend underscores a broader shift where weather-related risks are being aggressively priced into rates, often exceeding the $311 national average for property taxes.

Despite the high costs in disaster-prone areas, the report suggests that weather risk is not the sole determinant of premium levels, as state-level regulation plays a critical role in affordability. Interestingly, high-risk states like Florida, Louisiana, and California fall outside the top 20 for insurance as a share of housing costs, while states like Hawaii and Vermont maintain the lowest shares at 2.1% and 3.2%, respectively. While national rates surged by 45.8% between 2020 and 2025, there are signs of stabilization; the year-over-year increase slowed to 6% last year, down significantly from a 12.7% jump recorded in 2024.

Summary generated by RabbitReport AI from public reporting. The full article and original reporting belong to National Mortgage News.