Demand for LegalTech in Japan | Global Market Analysis Report

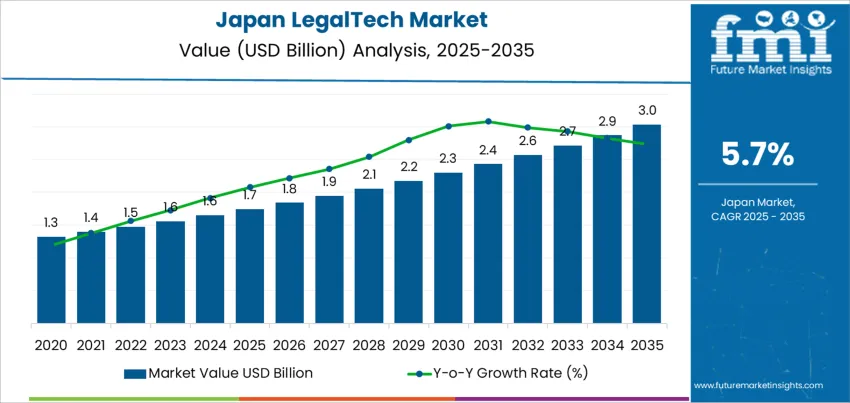

The Japanese LegalTech market is projected to grow from USD 1.80 billion in 2025 to USD 3.13 billion by 2036, representing a compound annual growth rate (CAGR) of 5.7%. This expansion is driven by a shift from conservative, paper-based workflows toward digital automation in response to labor constraints and mounting regulatory pressures. The market is expected to reach a significant inflection point between 2029 and 2031 as adoption spreads from large law firms to mid-sized enterprises and government bodies.

The market's trajectory is characterized by a back-loaded value creation model, where the most substantial absolute growth occurs in the later years of the forecast period. While the 2020–2025 phase saw modest gains of USD 0.4 billion, the 2030–2035 window is expected to add USD 0.7 billion as demand rises from USD 2.3 billion to USD 3.0 billion. Early adoption remains concentrated in contract management and e-discovery within large law firms, but the 2029–2031 inflection point will see spending accelerate due to the wider acceptance of cloud-based document automation and the need for Japanese language optimization in software tools.

Historically, Japan's LegalTech adoption was slowed by a reliance on physical documentation and strict professional boundaries, but structural shifts are now forcing a transition. A widening gap between increasing legal workloads and a shrinking, aging pool of legal professionals has made manual review unsustainable, particularly for cross-border trade requiring bilingual contract handling. Furthermore, Japanese courts and regulators have begun accepting digital filings, reducing the historical dependence on paper and encouraging investment in real-time risk monitoring and AI-driven document review.

In terms of solution format, deployment-based models dominate the market with a 62% share, as law firms and corporate departments prioritize direct software ownership and secure internal infrastructures for sensitive client data. Contract Lifecycle Management (CLM) represents the largest functional segment at 24% of total demand, followed by case management and document management systems. Procurement decisions are increasingly influenced by the need for cost control and reduced turnaround times, with vendors shifting strategies toward direct partnerships with domestic IT service firms to better integrate with existing enterprise resource planning systems.

Summary generated by RabbitReport AI from public reporting. The full article and original reporting belong to Future Market Insights.