FinTech Adoption Reshapes Bank Risk Profiles and Credit Allocation Strategies

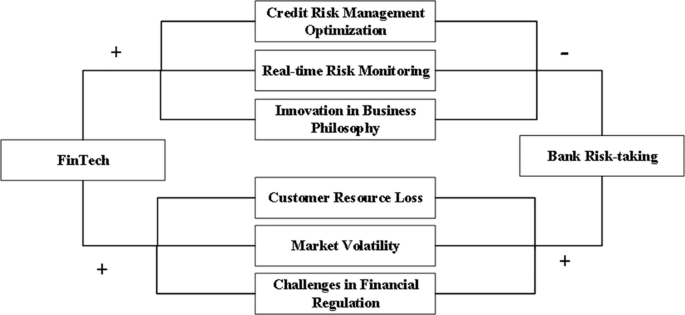

A comprehensive study of 587 commercial banks from 2015 to 2022 reveals that FinTech integration significantly alters how financial institutions manage risk and allocate credit. The research indicates that while technology encourages proactive risk-taking, it simultaneously reduces passive risk exposure, particularly within the micro, small, and retail lending sectors. These findings are vital for the banking sector as they highlight the dual nature of digital transformation in enhancing operational efficiency while requiring more sophisticated regulatory oversight.

Researchers Yun He and Wei Fan analyzed a dataset of 587 commercial banks over an eight-year period to determine how FinTech influences credit risk management and institutional stability. The study, published in Humanities and Social Sciences Communications, found that FinTech advancements allow banks to augment proactive risk-taking while curbing exposure to passive risks. This shift is attributed to the digitalization and automation of operations, which have fundamentally transformed traditional methods for information gathering, risk assessment, and investment decision-making. The research specifically highlights that the risk-preventive benefits of FinTech are most pronounced in regional banks, though the effectiveness varies depending on the specific geographical region of the institution.

The efficacy of FinTech tools varies significantly across different credit segments, according to the report. In the micro and small credit sectors, banks are leveraging big data analytics and artificial intelligence to assess creditworthiness with higher precision, thereby expanding the reach of these facilities. For retail lending, the implementation of automated approval processes and advanced credit scoring models has dramatically improved loan efficiency. However, the study notes that the risk-mitigating effects of FinTech are less pronounced in corporate credit, despite the application of blockchain and smart contracts intended to reduce information asymmetry and moral hazard.

The context of the study is centered on China, which the authors identify as a global leader in FinTech innovation and investment. Data from the China Financial Stability Report shows that by 2022, the non-performing loan (NPL) balance of banking institutions reached 2.98 trillion RMB, with an NPL ratio of 1.63%, representing a 1.55 trillion RMB increase since 2015. The researchers cite specific cases of systemic risk, such as irregular lending practices at Baoshang Bank and Henan Rural Commercial Bank, to illustrate the potential dangers of poorly managed digital expansion. Consequently, the study advises regulatory bodies to enhance their supervisory capabilities through regulatory technology (regtech) and encourages banks to refine their FinTech integration to preemptively mitigate systemic risks.

Summary generated by RabbitReport AI from public reporting. The full article and original reporting belong to Nature.