US Medical Devices Market Size to Hit USD 346.19 Billion by 2035

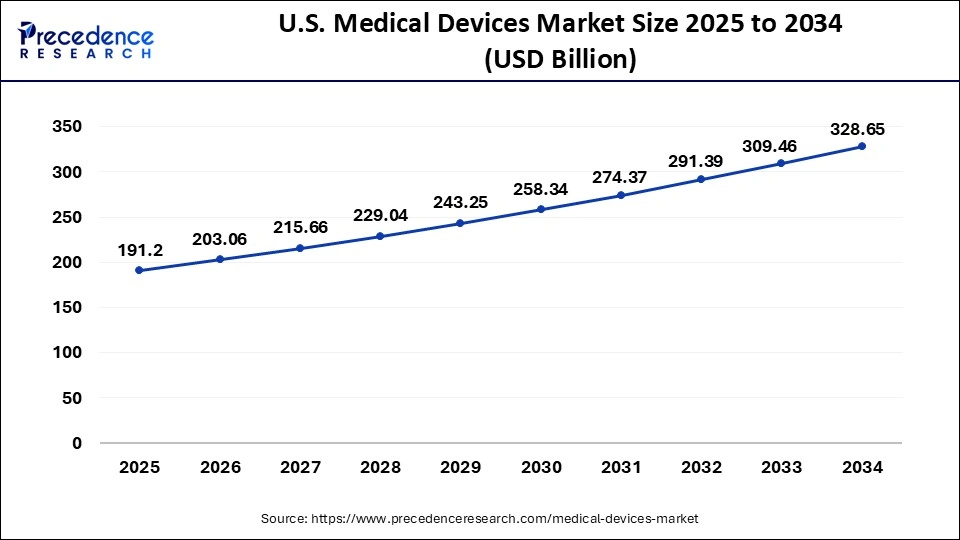

The United States medical devices market is projected to grow from USD 191.20 billion in 2025 to approximately USD 346.19 billion by 2035, representing a compound annual growth rate of 6.20%. This expansion is primarily driven by the integration of artificial intelligence, rising chronic disease prevalence, and a significant shift toward home healthcare settings. The sector's growth underscores a broader industry transformation toward precision medicine and the adoption of advanced robotic and diagnostic technologies.

The U.S. medical devices industry is entering a period of sustained growth, fueled by increasing healthcare expenditures and the rapid adoption of advanced technologies like AI-driven imaging and surgical robotics. Major players such as Medtronic, Johnson & Johnson MedTech, Intuitive Surgical, and Stryker are leading the market with new robotic platforms and sophisticated diagnostic software designed to improve clinical velocity and patient outcomes. The therapeutic devices segment remains the market leader as of 2025, supported by high procedure volumes in cardiology, orthopedics, and oncology, while the assistive and rehabilitation segment is poised for the fastest growth due to the needs of over 61 million American adults living with disabilities.

While hospitals currently dominate the market as the primary end-users—utilizing complex surgical systems and digital health platforms across more than 6,100 facilities—there is a notable shift toward home healthcare settings. This transition is supported by the increased uptake of digital health services and a growing preference for monitoring and treatment outside traditional clinical environments. Furthermore, while direct sales through specialized distribution networks remain the primary procurement method, online sales are expected to see the highest growth rate as healthcare providers digitize their procurement strategies.

California serves as a critical hub for the industry, hosting hundreds of medtech companies including Abbott, Edwards Lifesciences, and Penumbra, alongside over 400 hospitals and significant venture investment activity. However, the industry faces headwinds from stringent regulatory requirements and evolving compliance standards, which can increase development timelines and costs, particularly for small and medium-sized manufacturers. Additionally, ongoing supply chain vulnerabilities continue to influence operational planning and procurement strategies across the sector as manufacturers work to develop less traumatic, more efficient therapeutic solutions.

Summary generated by RabbitReport AI from public reporting. The full article and original reporting belong to Precedence Research.